Conditional Average Treatment Effects (CATE) with DoWhy and EconML

This is an experimental feature where we use EconML methods from DoWhy. Using EconML allows CATE estimation using different methods.

All four steps of causal inference in DoWhy remain the same: model, identify, estimate, and refute. The key difference is that we now call econml methods in the estimation step. There is also a simpler example using linear regression to understand the intuition behind CATE estimators.

All datasets are generated using linear structural equations.

[1]:

%load_ext autoreload

%autoreload 2

[2]:

import numpy as np

import pandas as pd

import logging

import dowhy

from dowhy import CausalModel

import dowhy.datasets

import econml

import warnings

warnings.filterwarnings('ignore')

BETA = 10

[3]:

data = dowhy.datasets.linear_dataset(BETA, num_common_causes=4, num_samples=10000,

num_instruments=2, num_effect_modifiers=2,

num_treatments=1,

treatment_is_binary=False,

num_discrete_common_causes=2,

num_discrete_effect_modifiers=0,

one_hot_encode=False)

df=data['df']

print(df.head())

print("True causal estimate is", data["ate"])

X0 X1 Z0 Z1 W0 W1 W2 W3 v0 \

0 -1.264829 1.477951 0.0 0.876127 -1.177224 2.162447 0 0 11.790429

1 0.285403 0.275850 0.0 0.674072 -0.564795 0.205294 2 3 24.917301

2 0.488269 2.793628 0.0 0.293566 -2.104491 2.133887 2 2 18.576141

3 1.128777 0.303312 0.0 0.585147 0.436949 1.515442 2 2 24.540409

4 -0.462207 0.576406 0.0 0.425401 -0.909995 -0.482890 3 1 17.510410

y

0 188.966111

1 307.304528

2 454.256152

3 322.503760

4 226.807535

True causal estimate is 14.545802196701313

[4]:

model = CausalModel(data=data["df"],

treatment=data["treatment_name"], outcome=data["outcome_name"],

graph=data["gml_graph"])

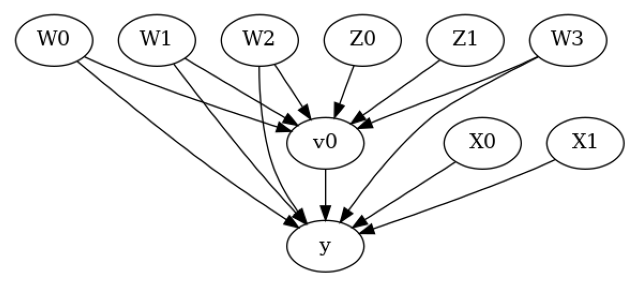

[5]:

model.view_model()

from IPython.display import Image, display

display(Image(filename="causal_model.png"))

[6]:

identified_estimand= model.identify_effect(proceed_when_unidentifiable=True)

print(identified_estimand)

Estimand type: EstimandType.NONPARAMETRIC_ATE

### Estimand : 1

Estimand name: backdoor

Estimand expression:

d

─────(E[y|W3,W1,W2,W0])

d[v₀]

Estimand assumption 1, Unconfoundedness: If U→{v0} and U→y then P(y|v0,W3,W1,W2,W0,U) = P(y|v0,W3,W1,W2,W0)

### Estimand : 2

Estimand name: iv

Estimand expression:

⎡ -1⎤

⎢ d ⎛ d ⎞ ⎥

E⎢─────────(y)⋅⎜─────────([v₀])⎟ ⎥

⎣d[Z₀ Z₁] ⎝d[Z₀ Z₁] ⎠ ⎦

Estimand assumption 1, As-if-random: If U→→y then ¬(U →→{Z0,Z1})

Estimand assumption 2, Exclusion: If we remove {Z0,Z1}→{v0}, then ¬({Z0,Z1}→y)

### Estimand : 3

Estimand name: frontdoor

No such variable(s) found!

Linear Model

First, let us build some intuition using a linear model for estimating CATE. The effect modifiers (that lead to a heterogeneous treatment effect) can be modeled as interaction terms with the treatment. Thus, their value modulates the effect of treatment.

Below the estimated effect of changing treatment from 0 to 1.

[7]:

linear_estimate = model.estimate_effect(identified_estimand,

method_name="backdoor.linear_regression",

control_value=0,

treatment_value=1)

print(linear_estimate)

*** Causal Estimate ***

## Identified estimand

Estimand type: EstimandType.NONPARAMETRIC_ATE

### Estimand : 1

Estimand name: backdoor

Estimand expression:

d

─────(E[y|W3,W1,W2,W0])

d[v₀]

Estimand assumption 1, Unconfoundedness: If U→{v0} and U→y then P(y|v0,W3,W1,W2,W0,U) = P(y|v0,W3,W1,W2,W0)

## Realized estimand

b: y~v0+W3+W1+W2+W0+v0*X0+v0*X1

Target units:

## Estimate

Mean value: 14.54571075193559

### Conditional Estimates

__categorical__X0 __categorical__X1

(-3.635, -0.4] (-3.3569999999999998, 0.0328] 6.738001

(0.0328, 0.624] 10.884184

(0.624, 1.129] 13.391808

(1.129, 1.716] 15.942846

(1.716, 4.932] 20.152733

(-0.4, 0.184] (-3.3569999999999998, 0.0328] 7.497401

(0.0328, 0.624] 11.566389

(0.624, 1.129] 14.088605

(1.129, 1.716] 16.653022

(1.716, 4.932] 20.751800

(0.184, 0.692] (-3.3569999999999998, 0.0328] 7.648464

(0.0328, 0.624] 11.935509

(0.624, 1.129] 14.554019

(1.129, 1.716] 17.109583

(1.716, 4.932] 21.116375

(0.692, 1.28] (-3.3569999999999998, 0.0328] 8.210322

(0.0328, 0.624] 12.459851

(0.624, 1.129] 14.993727

(1.129, 1.716] 17.534435

(1.716, 4.932] 21.836646

(1.28, 4.415] (-3.3569999999999998, 0.0328] 9.207287

(0.0328, 0.624] 13.083411

(0.624, 1.129] 15.696830

(1.129, 1.716] 18.219924

(1.716, 4.932] 22.366226

dtype: float64

EconML methods

We now move to the more advanced methods from the EconML package for estimating CATE.

First, let us look at the double machine learning estimator. Method_name corresponds to the fully qualified name of the class that we want to use. For double ML, it is “econml.dml.DML”.

Target units defines the units over which the causal estimate is to be computed. This can be a lambda function filter on the original dataframe, a new Pandas dataframe, or a string corresponding to the three main kinds of target units (“ate”, “att” and “atc”). Below we show an example of a lambda function.

Method_params are passed directly to EconML. For details on allowed parameters, refer to the EconML documentation.

[8]:

from sklearn.preprocessing import PolynomialFeatures

from sklearn.linear_model import LassoCV

from sklearn.ensemble import GradientBoostingRegressor

dml_estimate = model.estimate_effect(identified_estimand, method_name="backdoor.econml.dml.DML",

control_value = 0,

treatment_value = 1,

target_units = lambda df: df["X0"]>1, # condition used for CATE

confidence_intervals=False,

method_params={"init_params":{'model_y':GradientBoostingRegressor(),

'model_t': GradientBoostingRegressor(),

"model_final":LassoCV(fit_intercept=False),

'featurizer':PolynomialFeatures(degree=1, include_bias=False)},

"fit_params":{}})

print(dml_estimate)

2023-12-06 08:35:08.848732: I tensorflow/core/platform/cpu_feature_guard.cc:182] This TensorFlow binary is optimized to use available CPU instructions in performance-critical operations.

To enable the following instructions: AVX2 FMA, in other operations, rebuild TensorFlow with the appropriate compiler flags.

2023-12-06 08:35:10.987963: W tensorflow/compiler/tf2tensorrt/utils/py_utils.cc:38] TF-TRT Warning: Could not find TensorRT

*** Causal Estimate ***

## Identified estimand

Estimand type: EstimandType.NONPARAMETRIC_ATE

### Estimand : 1

Estimand name: backdoor

Estimand expression:

d

─────(E[y|W3,W1,W2,W0])

d[v₀]

Estimand assumption 1, Unconfoundedness: If U→{v0} and U→y then P(y|v0,W3,W1,W2,W0,U) = P(y|v0,W3,W1,W2,W0)

## Realized estimand

b: y~v0+W3+W1+W2+W0 | X0,X1

Target units: Data subset defined by a function

## Estimate

Mean value: 15.637000322550929

Effect estimates: [[12.3018562 ]

[20.34683672]

[16.6270295 ]

...

[11.96856018]

[17.78714676]

[ 4.99541676]]

[9]:

print("True causal estimate is", data["ate"])

True causal estimate is 14.545802196701313

[10]:

dml_estimate = model.estimate_effect(identified_estimand, method_name="backdoor.econml.dml.DML",

control_value = 0,

treatment_value = 1,

target_units = 1, # condition used for CATE

confidence_intervals=False,

method_params={"init_params":{'model_y':GradientBoostingRegressor(),

'model_t': GradientBoostingRegressor(),

"model_final":LassoCV(fit_intercept=False),

'featurizer':PolynomialFeatures(degree=1, include_bias=True)},

"fit_params":{}})

print(dml_estimate)

*** Causal Estimate ***

## Identified estimand

Estimand type: EstimandType.NONPARAMETRIC_ATE

### Estimand : 1

Estimand name: backdoor

Estimand expression:

d

─────(E[y|W3,W1,W2,W0])

d[v₀]

Estimand assumption 1, Unconfoundedness: If U→{v0} and U→y then P(y|v0,W3,W1,W2,W0,U) = P(y|v0,W3,W1,W2,W0)

## Realized estimand

b: y~v0+W3+W1+W2+W0 | X0,X1

Target units:

## Estimate

Mean value: 14.475725098861538

Effect estimates: [[15.99699218]

[11.45432521]

[23.79690413]

...

[20.39342015]

[ 5.07113297]

[20.89578696]]

CATE Object and Confidence Intervals

EconML provides its own methods to compute confidence intervals. Using BootstrapInference in the example below.

[11]:

from sklearn.preprocessing import PolynomialFeatures

from sklearn.linear_model import LassoCV

from sklearn.ensemble import GradientBoostingRegressor

from econml.inference import BootstrapInference

dml_estimate = model.estimate_effect(identified_estimand,

method_name="backdoor.econml.dml.DML",

target_units = "ate",

confidence_intervals=True,

method_params={"init_params":{'model_y':GradientBoostingRegressor(),

'model_t': GradientBoostingRegressor(),

"model_final": LassoCV(fit_intercept=False),

'featurizer':PolynomialFeatures(degree=1, include_bias=True)},

"fit_params":{

'inference': BootstrapInference(n_bootstrap_samples=100, n_jobs=-1),

}

})

print(dml_estimate)

*** Causal Estimate ***

## Identified estimand

Estimand type: EstimandType.NONPARAMETRIC_ATE

### Estimand : 1

Estimand name: backdoor

Estimand expression:

d

─────(E[y|W3,W1,W2,W0])

d[v₀]

Estimand assumption 1, Unconfoundedness: If U→{v0} and U→y then P(y|v0,W3,W1,W2,W0,U) = P(y|v0,W3,W1,W2,W0)

## Realized estimand

b: y~v0+W3+W1+W2+W0 | X0,X1

Target units: ate

## Estimate

Mean value: 14.463127900520695

Effect estimates: [[15.97361844]

[11.41717088]

[23.85464337]

...

[20.42508677]

[ 4.99954998]

[20.93700213]]

95.0% confidence interval: [[[15.91573366 11.3936291 23.76115269 ... 20.39889196 4.66546959

20.92996915]]

[[16.36499412 11.60290173 24.45769177 ... 20.89065299 5.28170646

21.42348094]]]

Can provide a new inputs as target units and estimate CATE on them.

[12]:

test_cols= data['effect_modifier_names'] # only need effect modifiers' values

test_arr = [np.random.uniform(0,1, 10) for _ in range(len(test_cols))] # all variables are sampled uniformly, sample of 10

test_df = pd.DataFrame(np.array(test_arr).transpose(), columns=test_cols)

dml_estimate = model.estimate_effect(identified_estimand,

method_name="backdoor.econml.dml.DML",

target_units = test_df,

confidence_intervals=False,

method_params={"init_params":{'model_y':GradientBoostingRegressor(),

'model_t': GradientBoostingRegressor(),

"model_final":LassoCV(),

'featurizer':PolynomialFeatures(degree=1, include_bias=True)},

"fit_params":{}

})

print(dml_estimate.cate_estimates)

[[10.61141168]

[11.44897072]

[12.8431554 ]

[13.08904521]

[11.12794764]

[10.31407202]

[14.46399892]

[13.56944939]

[15.03914465]

[11.12365802]]

Can also retrieve the raw EconML estimator object for any further operations

[13]:

print(dml_estimate._estimator_object)

<econml.dml.dml.DML object at 0x7f05e493e970>

Works with any EconML method

In addition to double machine learning, below we example analyses using orthogonal forests, DRLearner (bug to fix), and neural network-based instrumental variables.

Binary treatment, Binary outcome

[14]:

data_binary = dowhy.datasets.linear_dataset(BETA, num_common_causes=4, num_samples=10000,

num_instruments=1, num_effect_modifiers=2,

treatment_is_binary=True, outcome_is_binary=True)

# convert boolean values to {0,1} numeric

data_binary['df'].v0 = data_binary['df'].v0.astype(int)

data_binary['df'].y = data_binary['df'].y.astype(int)

print(data_binary['df'])

model_binary = CausalModel(data=data_binary["df"],

treatment=data_binary["treatment_name"], outcome=data_binary["outcome_name"],

graph=data_binary["gml_graph"])

identified_estimand_binary = model_binary.identify_effect(proceed_when_unidentifiable=True)

X0 X1 Z0 W0 W1 W2 W3 v0 y

0 -0.534052 1.093417 0.0 -1.795298 -0.143568 -0.366056 -0.109985 0 0

1 -1.410049 1.026043 0.0 0.492129 -0.119875 3.209130 0.941178 1 1

2 -1.050137 -0.021838 0.0 -0.429270 -0.737206 1.320258 0.804882 1 1

3 -1.587474 0.272291 0.0 -0.816793 -1.156613 0.506778 -0.009565 0 0

4 0.560242 2.063923 0.0 0.404508 -1.074329 -0.733262 -1.824770 0 0

... ... ... ... ... ... ... ... .. ..

9995 0.618577 1.331078 1.0 -2.185720 1.263190 -0.412815 -0.395641 0 0

9996 -1.108701 0.171365 1.0 0.974026 -1.133459 1.238863 0.097910 1 1

9997 0.961850 0.630912 0.0 0.881002 0.884787 -0.235011 0.272365 1 1

9998 -1.031732 1.089343 0.0 -0.846813 0.103321 0.483532 -1.245046 0 0

9999 -0.510225 0.689955 0.0 -0.299444 0.434148 -1.397242 -1.944962 0 0

[10000 rows x 9 columns]

Using DRLearner estimator

[15]:

from sklearn.linear_model import LogisticRegressionCV

#todo needs binary y

drlearner_estimate = model_binary.estimate_effect(identified_estimand_binary,

method_name="backdoor.econml.dr.LinearDRLearner",

confidence_intervals=False,

method_params={"init_params":{

'model_propensity': LogisticRegressionCV(cv=3, solver='lbfgs', multi_class='auto')

},

"fit_params":{}

})

print(drlearner_estimate)

print("True causal estimate is", data_binary["ate"])

*** Causal Estimate ***

## Identified estimand

Estimand type: EstimandType.NONPARAMETRIC_ATE

### Estimand : 1

Estimand name: backdoor

Estimand expression:

d

─────(E[y|W3,W1,W2,W0])

d[v₀]

Estimand assumption 1, Unconfoundedness: If U→{v0} and U→y then P(y|v0,W3,W1,W2,W0,U) = P(y|v0,W3,W1,W2,W0)

## Realized estimand

b: y~v0+W3+W1+W2+W0 | X0,X1

Target units: ate

## Estimate

Mean value: 0.3066723343496284

Effect estimates: [[0.35136016]

[0.21415875]

[0.2214162 ]

...

[0.55928025]

[0.27497376]

[0.33658516]]

True causal estimate is 0.3568

Instrumental Variable Method

[16]:

dmliv_estimate = model.estimate_effect(identified_estimand,

method_name="iv.econml.iv.dml.DMLIV",

target_units = lambda df: df["X0"]>-1,

confidence_intervals=False,

method_params={"init_params":{

'discrete_treatment':False,

'discrete_instrument':False

},

"fit_params":{}})

print(dmliv_estimate)

*** Causal Estimate ***

## Identified estimand

Estimand type: EstimandType.NONPARAMETRIC_ATE

### Estimand : 1

Estimand name: iv

Estimand expression:

⎡ -1⎤

⎢ d ⎛ d ⎞ ⎥

E⎢─────────(y)⋅⎜─────────([v₀])⎟ ⎥

⎣d[Z₀ Z₁] ⎝d[Z₀ Z₁] ⎠ ⎦

Estimand assumption 1, As-if-random: If U→→y then ¬(U →→{Z0,Z1})

Estimand assumption 2, Exclusion: If we remove {Z0,Z1}→{v0}, then ¬({Z0,Z1}→y)

## Realized estimand

b: y~v0+W3+W1+W2+W0 | X0,X1

Target units: Data subset defined by a function

## Estimate

Mean value: 14.805808316112596

Effect estimates: [[11.69568463]

[24.05624296]

[12.39538056]

...

[20.64670216]

[ 5.13271463]

[21.08361933]]

Metalearners

[17]:

data_experiment = dowhy.datasets.linear_dataset(BETA, num_common_causes=5, num_samples=10000,

num_instruments=2, num_effect_modifiers=5,

treatment_is_binary=True, outcome_is_binary=False)

# convert boolean values to {0,1} numeric

data_experiment['df'].v0 = data_experiment['df'].v0.astype(int)

print(data_experiment['df'])

model_experiment = CausalModel(data=data_experiment["df"],

treatment=data_experiment["treatment_name"], outcome=data_experiment["outcome_name"],

graph=data_experiment["gml_graph"])

identified_estimand_experiment = model_experiment.identify_effect(proceed_when_unidentifiable=True)

X0 X1 X2 X3 X4 Z0 Z1 \

0 1.123930 3.022222 -2.109433 1.328408 -0.840823 1.0 0.129756

1 1.170840 -0.146780 -0.075093 0.175070 -1.536037 0.0 0.040805

2 -0.125031 1.019724 0.711940 1.782758 -1.349459 0.0 0.723018

3 0.558548 -0.440357 -2.302349 0.622907 -0.121145 1.0 0.895617

4 0.531709 -0.699705 1.129274 1.832657 -0.048803 1.0 0.909017

... ... ... ... ... ... ... ...

9995 -1.189891 0.682024 -0.842743 -1.992564 -1.324105 0.0 0.989291

9996 0.728924 -0.641323 -1.420311 1.217292 -0.844110 1.0 0.318631

9997 0.854360 -0.350899 -0.437845 0.219528 -0.070029 0.0 0.871692

9998 -0.015274 0.875106 0.110283 2.613046 0.361263 0.0 0.374467

9999 1.421508 -0.112686 1.515643 0.511508 -0.292077 1.0 0.958921

W0 W1 W2 W3 W4 v0 y

0 0.715142 -1.187774 -1.200612 -1.533813 0.776998 1 10.341688

1 1.005776 0.241121 -0.300989 1.710419 2.455758 1 29.654986

2 -2.111568 -0.906330 2.349031 -2.285756 0.161132 1 0.536233

3 -1.424980 -0.751965 -2.018740 0.558397 1.125804 1 -3.399556

4 -1.988515 -2.628349 -0.713607 -0.378804 0.594590 1 -1.203633

... ... ... ... ... ... .. ...

9995 -1.209167 -1.208427 0.779056 0.994410 2.085716 1 7.089060

9996 0.198992 1.151383 0.363411 -0.938753 2.147780 1 13.943921

9997 -0.587188 -0.903376 0.877840 0.293941 0.779997 1 15.648287

9998 -0.742580 -3.215314 -1.095717 -0.499757 -0.147348 0 -17.576172

9999 0.965338 -0.029347 2.055957 -0.826532 -0.636682 1 24.912374

[10000 rows x 14 columns]

[18]:

from sklearn.ensemble import RandomForestRegressor

metalearner_estimate = model_experiment.estimate_effect(identified_estimand_experiment,

method_name="backdoor.econml.metalearners.TLearner",

confidence_intervals=False,

method_params={"init_params":{

'models': RandomForestRegressor()

},

"fit_params":{}

})

print(metalearner_estimate)

print("True causal estimate is", data_experiment["ate"])

*** Causal Estimate ***

## Identified estimand

Estimand type: EstimandType.NONPARAMETRIC_ATE

### Estimand : 1

Estimand name: backdoor

Estimand expression:

d

─────(E[y|W3,W1,W2,W0,W4])

d[v₀]

Estimand assumption 1, Unconfoundedness: If U→{v0} and U→y then P(y|v0,W3,W1,W2,W0,W4,U) = P(y|v0,W3,W1,W2,W0,W4)

## Realized estimand

b: y~v0+X3+X0+X2+X4+X1+W3+W1+W2+W0+W4

Target units: ate

## Estimate

Mean value: 18.742046322509356

Effect estimates: [[19.90968305]

[28.05921386]

[15.12991291]

...

[20.25646756]

[17.54863467]

[26.25831746]]

True causal estimate is 11.548902280318803

Avoiding retraining the estimator

Once an estimator is fitted, it can be reused to estimate effect on different data points. In this case, you can pass fit_estimator=False to estimate_effect. This works for any EconML estimator. We show an example for the T-learner below.

[19]:

# For metalearners, need to provide all the features (except treatmeant and outcome)

metalearner_estimate = model_experiment.estimate_effect(identified_estimand_experiment,

method_name="backdoor.econml.metalearners.TLearner",

confidence_intervals=False,

fit_estimator=False,

target_units=data_experiment["df"].drop(["v0","y", "Z0", "Z1"], axis=1)[9995:],

method_params={})

print(metalearner_estimate)

print("True causal estimate is", data_experiment["ate"])

*** Causal Estimate ***

## Identified estimand

Estimand type: EstimandType.NONPARAMETRIC_ATE

### Estimand : 1

Estimand name: backdoor

Estimand expression:

d

─────(E[y|W3,W1,W2,W0,W4])

d[v₀]

Estimand assumption 1, Unconfoundedness: If U→{v0} and U→y then P(y|v0,W3,W1,W2,W0,W4,U) = P(y|v0,W3,W1,W2,W0,W4)

## Realized estimand

b: y~v0+X3+X0+X2+X4+X1+W3+W1+W2+W0+W4

Target units: Data subset provided as a data frame

## Estimate

Mean value: 18.71229118037352

Effect estimates: [[14.69208446]

[14.80595175]

[20.25646756]

[17.54863467]

[26.25831746]]

True causal estimate is 11.548902280318803

Refuting the estimate

Adding a random common cause variable

[20]:

res_random=model.refute_estimate(identified_estimand, dml_estimate, method_name="random_common_cause")

print(res_random)

Refute: Add a random common cause

Estimated effect:12.363085365933857

New effect:12.341220390740773

p value:0.46

Adding an unobserved common cause variable

[21]:

res_unobserved=model.refute_estimate(identified_estimand, dml_estimate, method_name="add_unobserved_common_cause",

confounders_effect_on_treatment="linear", confounders_effect_on_outcome="linear",

effect_strength_on_treatment=0.01, effect_strength_on_outcome=0.02)

print(res_unobserved)

Refute: Add an Unobserved Common Cause

Estimated effect:12.363085365933857

New effect:12.325334320191756

Replacing treatment with a random (placebo) variable

[22]:

res_placebo=model.refute_estimate(identified_estimand, dml_estimate,

method_name="placebo_treatment_refuter", placebo_type="permute",

num_simulations=10 # at least 100 is good, setting to 10 for speed

)

print(res_placebo)

Refute: Use a Placebo Treatment

Estimated effect:12.363085365933857

New effect:0.012137033388297663

p value:0.31953547192756526

Removing a random subset of the data

[23]:

res_subset=model.refute_estimate(identified_estimand, dml_estimate,

method_name="data_subset_refuter", subset_fraction=0.8,

num_simulations=10)

print(res_subset)

Refute: Use a subset of data

Estimated effect:12.363085365933857

New effect:12.315879364150556

p value:0.03437419719145829

More refutation methods to come, especially specific to the CATE estimators.